How do companies raise money?

Uber. Snap, Spotify. Tesla. Dropbox.

All of these companies are valued at billions and yet none of them have ever posted a profit. They’ve survived – and grown – because they’ve raised huge sums of money from investors. Without that finance, they’d die.

Many other companies need to raise money in the early days. It can be hard to start a business – to buy equipment, hire staff and get customers – from savings or money from family and friends.

Even as they become established, companies continue to raise money to buy other companies, open up overseas or invest in new technology. Raising money allows these companies to invest in growth and free up cash to spend elsewhere.

Equity and Debt

For an interview, you don’t need to know all the different ways to finance a business, but you should understand the two categories that they fall into – equity or debt. (Note, they sometimes come under both, but we’ll touch on that another time).

What is equity finance?

Imagine that you’re the sole founder of Company X. At this point, no-one else has invested in your company.

We say that you own 100% of the shares in Company X.

You can think of a share as a piece of ownership in the company. In this case, you own all the pieces.

Now let’s say you want to raise money.

One option you have is equity finance. This is where you sell some of those pieces of ownership in your company – some shares – to raise money.

Suppose you decide to go down this route. It takes a lot of time and many presentations, but eventually, you find a willing investor. The investor offers to give you a chunk of money for a 30% stake in Company X.

Let’s think about the benefits and costs of this deal.

The benefits of equity finance

- There are few restrictions on how the cash is spent.

- There’s no loan to repay.

- You don’t have to pay any interest.

- You don’t have to pay the investor back, even if Company X becomes insolvent.

The costs of equity finance

- The investor now co-owns your business and it’s likely that it’ll be that way for a long time.

- The investor has some control. Normally, one share is equal to one vote, so the investor has 30% of the votes in the company, which gives him considerable influence over how the company is run.

- The investor will want to exit at some point. You may not be on a repayment schedule, but the investor did invest in your company to see a return. This may affect your company strategy, for example, an investor may want to sell when you don’t.

- The investor will share the returns of any dividends and/or in the event of an exit. Dividends – payments made by from company profits to shareholders – don’t have to be paid, but if they are, the investor will be entitled to a share. The same applies to a sale or initial public offering, so you could effectively be paying out much more to an investor than you originally thought.

There are also practical considerations when it comes to issuing equity. In reality, it’s not easy to find an investor, which makes it – unlike debt – time-consuming and costly.

Note that for larger companies, the story is a little different. They head to a market to sell their shares – the equity capital markets. I’ll save the detail for a future newsletter, but in short, the equity capital markets provide a company with access to a big pool of investors and a lot more money. But there are also many costs and risks, including strict regulation, disclosure requirements, penalties and liability risks.

What is debt finance?

It means borrowing money. The money must be repaid within a specified period of time, usually with interest.

We’ll focus on two forms of debt finance: loans and bonds.

Raising money through loans

Imagine you’re a business owner. You ask the bank for a loan.

The bank asks you lots of questions about your company – why you need the money, how much money and profit you’ve made over the last few years, what your assets are, and how you’ll pay the loan back.

Even with all of that information, there’s a risk that you won’t be able to pay the money back. Maybe, you overestimated how much a client would pay you, or perhaps a bad review deters future customers.

But that’s not the bank’s problem. They want to know they can get their money back, especially if things go wrong.

So, the bank asks you to give something up if you can’t pay the loan back. That could be one of your factories or some equipment – whatever equals the value of the loan. Then, if you do default on your loan, the bank has the right to sell those assets to get its money back.

If this happens, we say the bank has security. You have a secured loan.

Suppose the bank agrees to lend you the money. You’ll pay the loan back in instalments over a number of years. You’ll also pay a little extra, which is the interest on the loan. That way, the bank makes a profit from lending to you.

If you’re asking for a lot of money, a single bank may not be willing to risk lending the entire amount. In that case, the bank may partner up with another lender, and they’ll both lend you the money.

If there are multiple lenders providing the loan together, it’s called a syndicated loan.

Raising money by issuing bonds

A bond is like a loan split up into many chunks.

If you issue bonds, you are borrowing small amounts of money from many investors. In return, you promise to pay interest to the investors periodically, and, at the end of a specified date, you promise to pay back the original sum.

Bonds can be issued to the public or they can be issued privately. A public issue is good if you want to raise a lot of money and have access to a wide pool of investors. Investors can then sell your bond to other investors in secondary markets if they want their money back early. These bonds will be graded, which tells investors how likely it is that you’ll fail your debts.

But there are also costs involved. Public bond issues are subject to a lot of rules.

You’ll have to reveal a lot of information about your company and the risks of investing in your bonds.

This can be too expensive and time-consuming. So, sometimes, it’ll be better to issue bonds privately. The bonds will be sold to a select group of experienced investors. They should be more interested in keeping the bond because the secondary market will be limited.

Note, so far we’ve been talking about corporate bonds.

Governments can also issue bonds to raise money. UK government bonds are called gilts. US government bonds are called treasury bonds. These are safer investments; you can generally trust a government not to default. But these bonds also pay less interest.

Why loans instead of bonds?

- It’s quicker to get a loan.

- The terms of a loan will be private.

- You can get flexible loan terms.

- They’re suitable for a variety of companies, not just those over a certain size.

Why issue bonds instead of getting a loan?

- They’re often cheaper (you can pay a lower interest rate).

- You have more freedom to spend the money.

- There are fewer and less stringent restrictions on your company. We call these restrictions covenants.

- They’re a viable option for companies with a lower credit rating. These companies can issue junk bonds.

Keep an eye out for Part 3 where we’ll be comparing equity and debt finance!

What is Private Equity? A Complete Guide for Law Students

If you’re applying to and interviewing at private-equity-focused firms, you can expect to be asked questions to test your understanding of what it is, how it works, and the role of lawyers in this sector.

This guide has two primary aims: 1) to provide you with the information you need to excel at interviews with a private equity focus and 2) to teach you about private equity in an easy-to-understand manner. Structured through a series of practice interview questions, you’ll gain an understanding of private equity and learn how to articulate your answers to challenging interview questions.

This guide will also be useful if you are beginning a vacation scheme at one of these firms and want to refresh your memory, or if you want to express an interest in private equity at a general interview, and seek to be able to handle possible follow up interview questions.

For some questions, the points to note will help you to formulate your answer to the interview question, whereas the bonus information is designed to give you additional knowledge about the topic. You wouldn’t be expected to know much of this bonus information, but they may help you to handle follow up questions.

A note on the sample interview answers: these answers should be used as guidance rather than scripted answers. Why? Firstly, the aim of this guide is to teach you about private equity through a series of interview questions, which is why a lot of these answers are far more detailed than you would be expected to give in an interview answer. Second, most points carry across well in text but don’t convey how they should be said in an interview where delivery and tonality is important. Scripted answers are easy to see!

Mock Interview Answers

Interview Question: Why are you interested in private equity?

Points to Note: Private equity accounts for a substantial amount of income for some of the top US law firms in London. Their practice areas are often positioned to service the needs of these private equity clients, whether it’s assisting in the fundraising process, driving the deals, or in supporting clients on an advisory basis.

At these firms, as private equity will account for much of your day-to-day work as a lawyer, a recruiter will want to know: Do you have a genuine interest in this area? Will it excite you in the long term? Is your interest enough to keep you working the demanding hours associated with private equity work?

Equally, as a very lucrative sector, private equity is a core strength of some of the largest firms in London. If you do have an interest in private equity and decide to express that in your application or interview, it is important you are able to express why that is the case.

In these sample answers, we want to interweave your interest with a clear understanding of private equity.

Sample Answer: I am interested in private equity because…

- The clients: I like how private equity clients are unlikely typical corporate clients. Due to the nature of private equity, clients will be experienced in raising funds and completing deals under high pressure and within a short period of time. What this means for me as a lawyer is that I’ll be dealing with smart and sophisticated clients; clients who know what they want and what to expect from their lawyers. I am the kind of person that thrives under this high intensity environment, and I feel working in private equity will push me outside my comfort zone.

- Speed of transactions: I like how private equity moves at a very fast pace. As time plays an important role* in the success of a private equity firm, deals must be completed under a relatively shorter time frame compared to normal corporate transactions. This means I’ll likely be working on a number of deals at any one time and potentially complete more deals than I would normally have the opportunity to in a typical corporate seat. I feel this offers a steeper learning curve, which is important to me in my career, allowing me to develop into a more experienced commercial lawyer.

- Commercial interest: My interest in private equity aligns with why I wanted to be a commercial lawyer in the first place. It’s exciting how private equity firms seek to create value in companies, and invest and acquire businesses at some of the most critical points in their development. I’ll gain a real insight into what makes businesses tick and how they compete in the market to gain a competitive advantage. These deals will also often be crucial for the portfolio companies in their next stage of growth, and it might lead to working on some of the most complex transactional deals I can expect to see.

- Variety: As private equity firms invest in companies across different sectors, geographies and lifecycles, I feel working in private equity will offer a level of variety that I wouldn’t see in other practice areas. I find it exciting how one day I might be working on a deal for a high-growth tech company, while the next may be dealing with issues for a distressed retail business. This will make my day to day to work continuously new and interesting.

Interview Question: What is private equity?

Sample Answer: Private equity is:

- The investment of capital in (usually) private companies in return for an equity stake (shares in the business).

- The way this works is private equity firms raise money from investors* which is pooled into a fund. The fund will identify companies which they believe they can improve, perhaps because they’re fast-growing, in trouble, or not being run in the most efficient way possible. They’ll aim to sell these companies to generate a return for themselves and their investors.

* The investors we are referring to here tend to be institutional investors, which are investors with huge amounts of money to invest, such as insurance companies or pension funds.

Interview Question: What do you think makes private equity unique and different to other funds?

Sample Answer: I think private equity is unique because…

- It’s long term capital: When investors give their money* to a private equity firm, it’s locked up for the long term. With an average lifespan of ten years, investors to a private equity fund lose the ability to invest their money elsewhere. This gives private equity funds the space, time and control to make long-term investments – buying, improving and then selling a variety of portfolio companies. This is why the investors to a private equity fund also tend to be sophisticated.

- Private equity funds are closed: Once investors give their money, they cannot get their money back as and when they demand. Instead, they receive money when the portfolio companies are sold. This is unlike many other types of funds where you can invest or exit when you want.

- Blind pool: While investors may know the broad remit of a private equity fund, they commit capital on a ‘blind pool’ basis, which means they have little say on the individual acquisitions a private equity fund will make.

- High risk/returns: Private equity typically beats most benchmark indices, making it a popular choice for investors like pension funds who seek to allocate a proportion of their assets to funds that can generate a higher return. This comes with risks, however, as investors this is a long-term investment in an illiquid asset class (investors can’t take their money out easily).

Interview Question: What is a private equity fund?

Sample Answer: A fund is…

- A vehicle for a private equity firm to pool together money from investors (together with its own money) and invest in companies.

Bonus Information:

- Private equity funds are typically set up as limited partnerships, and the investors who invest in private equity funds are called limited partners. They are passive investors, which means they aren’t involved in the day to day running of the fund. In return, they get the benefit of limited liability, which means they are only liable for the money they invested.

- The private equity firm serves as the general partner and is responsible for managing the fund and its investments. The general partner owes duties to the limited partners and, unlike the limited partners, are personally liable for the debts and liabilities of the fund.

- The general partners will contribute a small percentage of their own capital to the fund. This gives them skin in the game, aligning their interests with that of the limited partners, because they are incentivised to achieve returns.

- It is the Limited Partnership Agreement that sets out the relationship between the general partners and limited partners.

- A private equity fund does not receive all the money from investors upfront. Instead, investors will commit to invest a certain amount, the total of which we call committed capital. The private equity fund will then issue capital calls when it needs the money to make purchases.

Interview Question: What is a buyout?

Sample Answer: In the context of private equity, a buyout is…

- Where a private equity firm acquires a controlling stake (over 50% of shares) in a company.

Bonus Information:

We’re concentrating on buyouts here as, at the firms you’re applying to, these are the kind of investments private equity firms will make. Note, however, that private equity can take different forms and there are a large variety of funds with different strategies and focuses. For example, a venture capital fund will tend to make minority stake investments in small, early stage companies. There are even funds of funds, which are funds that invest in other private equity funds. That way, a private equity investor will have a diversified investment portfolio across multiple funds.

There are also different types of buyouts. If the existing management of a company wants to buy it out with the support of a private equity firm, this is called a management buyout or MBO. If a private equity firm seeks to buy a company and bring in new management, we call this a management buy in or MBI.

We’re most concerned with institutional buyouts, where a private equity firm initiates the buyout.

Interview Question: What is a leveraged buyout?

Sample Answer: A leveraged buyout is…

- Where a private equity firm acquires a controlling stake (over 50% of shares) in a company, using a high proportion of borrowed money (debt).

Bonus Information:

Again, at many of the top commercial firms, the types of buyouts you can expect to work on will be leveraged.

Because of the high amount of debt being used, private equity firms will want to invest in companies with a strong cash flow. They can then use the cash flow of the company to pay off the interest payments. This does come with risks, but it also has the effect of encouraging management to be efficient and have a better handle of their costs – to be able to service the debt payments.

Even More Bonus Information (don’t worry, you won’t be expected to know this!):

Due to the sums involved, private equity firms may borrow money from a variety of lenders to finance the acquisition. The largest will often be from one or more banks, which is called senior debt. The transaction will be structured in a way that ensures they have priority when it comes to being paid interest. They’ll also often be given security, which gives them the right to repossess assets if the company fails to pay its interest. Junior debt may also be involved, in the form of mezzanine financing or high yield bonds. They are further along the chain when it comes to receiving interest payments and they typically don’t have security over the assets of the company.

Interview Question: Why use leverage?

Sample Answer: Leverage is used because…

- It frees up capital: The private equity firm can use less money from the fund, which therefore frees up capital to purchase other companies.

- Increases the rate of return:

- It has tax benefits: The interest payments on the borrowed money can be netted against the earnings of the company.

Interview Question: How do private equity firms influence the companies they acquire?

Points To Note:

A key distinction between typical M&A deals and private equity transactions comes down to what happens after an acquisition takes place. Private equity firms buy companies with the intention to improve them and then sell them again, typically within three to seven years. To be able to improve the companies they buy, it’s important for private equity firms to have influence over the companies they acquire.

A private equity firm might influence the companies by…

- Acquiring a controlling stake: Private equity firms will seek to buy over 50% (and often 100%) of the shares of the companies they acquire. With this ownership stake, they will have the ability to appoint and remove directors, giving them influence over the running of the company.

- Aligning incentives: Private equity firms tend to give management a compensation plan that gives them an ownership stake in the company. This means the management are incentivised to work with the private equity firm.

- Board approval: Partners from the private equity firm may join the board of the company and/or appoint outside advisers. Importantly, this will give them influence over important decisions, which may require approval of the board – such as selling assets, spending increases etc.

Interview Question: How do private equity firms add value to the companies they acquire?

Points To Note:

Remember, the pitch of private equity firms is that they have the tools, knowledge and resources to buy companies, improve them, and sell them for a greater return.

Sample Answer:

- Private equity firms undertake substantial research before buying a company. This means they’ll typically have already identified areas for improvement before the acquisition.

- The way they improve the company depends on that particular company; it may be to install new management, restructure the debt of a company, bring in experts to scrutinise the financials of a company and build financial models, invest in new technology, identifying trends and underperforming companies, selling off assets, buy other businesses, improve existing processes and streamlining operations, or leverage more debt.

- Importantly, private equity firms bring in their expertise and relationships, having worked with a substantial number of companies in the past.

Interview Question: How is the success of a private equity fund measured?

Sample Answer: The success of a fund is measured by:

- Its internal rate of return: This is the return on capital generated by a fund over a particular period (minus the fees of the firm).

Bonus Information:

You don’t need to worry about the calculation of the internal rate of return as it’s complicated, but note that it’s the most important ranking for a private equity fund. Because it’s based on a period of time, this is why private equity firms seek to generate a return and sell a company quickly.

There are other metrics to also measure the success of a fund, but we don’t need to worry about them here.

Interview Question: How do private equity firms make their money?

Sample Answer: Private equity firms make their money through:

- Carried interest: A share of the fund’s net profits (typically 20%) is paid to the general partner.

- Management fee: The limited partners also pay annual management fees (typically 2% of committed capital) to cover the day to day expenses/overheards of the private equity firm.

Bonus Information:

Carried interest or ‘carry’ is how a private equity firm generates wealth.

The Limited Partnership Agreement will set out how the money is distributed between the general partner and limited partners. Typically, the limited partners receive a minimum rate of return first before the carried interest is paid to the general partner.

Interview Question: What is ‘dry powder’?

Sample Answer: In the context of private equity…

- Dry powder refers to money that has been ‘committed’ by investors but is yet to be invested.

Bonus Information:

As discussed above, rather than receiving money upfront, a general partner draws down on the money from its investors over the course of a fund, making capital calls as and when it is ready.

You might have seen the phrase ‘dry powder’ frequently referenced in the news. For some time now, private equity firms have accumulated record levels of unspent cash (as of December 2019, this hit $2.5tn across all fund types, according to Bain & Co).

Commercial Awareness Update May 2018

Welcome to Part 1 of our commercial awareness update for May 2018

![]()

BT’s radical cost-cutting plan

- The story: In one of its biggest transformations in a decade, BT is cutting 13,000 jobs in a bid to reduce costs and improve investor confidence in the company. In early 2017, BT was fined the largest penalty ever imposed by Ofcom for breaching contracts with telecoms providers, and recently, Ofcom warned BT that unless it invests more into full-fibre networks, it’ll be at risk of ‘fading away’. Later in 2017, BT was also fined £225m for an accounting scandal within its Italian operations.

- Impact on law firms and clients: BT dominates the UK broadband market through its subsidiary, Openreach, but for years the communications regulator, Ofcom, has been putting pressure on BT to adapt. Ofcom’s warning that BT should invest in new technology comes as a recent report revealed that the UK lags far behind Europe on broadband speed. The story sheds light on the competition and regulatory issues that businesses face when they are effectively monopolies and own large shares of their markets.BT will also need to be wary of employment legislation and undertake consultations with unions to minimise any legal or reputational risks during the redundancies. BT is already dealing with the second-worst funded pension scheme in the world, which poses a significant liability for the business.

The US-China trade war

- The story: There’s never a dull day when it comes to Trump’s negotiations with China. His demands call for, among other things, China to reduce their tariffs, narrow their trade surplus with the US, remove their state subsidies for certain industries, and lift their restrictions on foreign companies doing business in China. The two countries are currently in trade talks after Trump lifted US sanctions on Chinese telecoms company ZTE, allowing it to resume operations (despite the company pleading guilty to illegally shipping US goods to Iran).

- Impact on law firms and clients: If China concedes on these trade demands, it should be a good thing for foreign businesses and law firms. China has already announced that it’ll open its market for financial services and the automobile sector, and under the new terms, there’s scope for China to allow foreign firms to do business in the country without having to set up a joint venture with a Chinese partner. So far, these restrictions have limited the ability of law firms to do business in the region, so if they’re lifted, it opens up a variety of legal work both in and out of the country.

Takeda Pharmaceutical Co. to acquire rival Shire

- The story: If it goes through, the $46bn deal to acquire Shire will be the largest ever acquisition by a Japanese company and place Takeda among the top global pharmaceutical companies by revenue. It’ll also give the Japanese company entry into the lucrative US market, where much of Shire’s business takes place.

- Impact on law firms and clients: The healthcare sector is a huge market for M&A lawyers and it’s set to boom in 2018 thanks to US tax reform, the costs of bringing a new drug to market, existing drugs going off patent and competition from generic drug firms. In the healthcare sector, M&A offers a fast growth strategy and a way to access an immediate pipeline of drugs.

HSBC’s road to recovery

- The story: From Mexican money laundering to failed acquisitions, HSBC has had its fair share of scandals over the last few years. Just recently, the firm put aside $897m to cover costs relating to the mis-selling of mortgage products before the financial crisis and, as a result, HSBC announced a fall in pre-tax profits for the first quarter of 2018.

- Impact on law firms and clients: Banks have had to spend billions to settle regulatory fines for their activities before, during and after the financial crisis, and then some more to overhaul their systems. This is likely to have squeezed the legal budgets for some banks forcing law firms to consider alternative fee arrangements, such as fixed fees, so they can keep their roles as legal advisers. On the flipside, these fines have led to a high volume of work for financial regulation and regulatory and investigation teams within law firms.

Carillion report criticises accounting firms and legal advisers

- The story: In a recent MP report, three magic circle law firms, several US firms and the big four accountancy firms were criticised for “squeezing fee income” out of Carillion, the recently collapsed government contractor. The big four were also criticised for turning a blind eye to what was going on at Carillion and pocketing large sums in the process.

- Impact on law firms and clients: The collapse of Carillion is one of the biggest British company failures in recent years and it has since created a host of work for restructuring, insolvency, employment and litigation lawyers. The report also made several critical suggestions. It asked the Insolvency Service to check whether the former directors at Carillion could be disqualified for breaching their duties under the Companies Act. It also called for the big four accountancy firms – KPMG, PWC, EY and Deloitte – to be referred to the UK regulator, the Competition and Markets Authority, to determine whether they should be broken up. This would be a radical shake-up in the industry and the accountancy firms have already begun to draft contingency plans.

[blog_teaser title=”” title_tag=”h3″ category=”” category_multi=”” margin=”1″]

What skills do the next generation of lawyers need?

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

Our resident law-tech enthusiast, Jonty, writes about his experience attending Legal Cheek’s The Future of Legal Education and Training Conference held on Wednesday 23 May 2018. The original forum post can be found here.

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

I was lucky enough to get taken along to this all day conference yesterday which featured both a cracking guest list and free breakfast & lunch, an all-round win really.

I thought you may find it helpful to hear a little bit about some of the things that were mentioned, as it’ll directly affect you all in the near future. You have to bear with me though, I lost some of my notes from the day so there will be parts mostly from memory.

Session 1

The morning session was all short talks (around 10 minutes) about innovation in the industry & what kind of future it may hold.

We heard from David Halliwell (Director of Knowledge & Innovation Delivery at Pinsent Masons) who spoke at length about how the roles within law are changing. He pointed some of the roles now available include legal technologists, legaltech project managers and legal engineers (although Scottish firm Cloch Solicitors are trying to trademark the term apparently, so be careful how you use it!). He went on to talk about how this reflects the move in the industry from the traditional route and how it may well open up to a point where we have far, far more roles on offer within law firms.

Next up was Isabel Parker (Chief Legal Innovation Officer at Freshfields) who spoke on the topic of diversity, namely cognitive diversity. The idea of pushing creativity within firms, rather than mechanical operatives. She mentioned the need to look for out of the box candidates, rather than hiring within their own image. So, on that note, I think we can expect more and more paths to pop up as the magic circle and others look for a different kind of thinker.

Parker also spoke about the need for law firms to encourage more people to get involved with technology but also to allow solicitors in firms the freedom to play (and fail) with technology. On that note, David Halliwell spoke about how Pinsent Masons have set up a programme which allows solicitors to have a coupon inhouse which counts as a “discount” against their billable hours targets, thus hours they plug into lawtech sessions are hours they don’t have to try to make up elsewhere.

Third session was from Shruti Ajitsaria (Head of Fuse at Allen & Overy). Shruti was probably my favourite speaker of the day and is generally just a great source of friendly information – if any of you want something to put on your CV you may want to look into (politely) contacting her to find out if you can go down to Fuse to see what they do down there, as she mentioned she was open to the idea yesterday of solicitors coming in and I doubt she would mind law students contacting her too.

Shruti spoke about how she got to opening Fuse after working as a derivatives solicitor at A&O for a long time and becoming frustrated at the lack of tech coming through. She mentioned an example of frustration during the GFC. A&O had a ton of derivatives agreements, which were created in Microsoft Word, printed off, signed and filed away somewhere. They had thousands of these, with 90% of them being pretty standard with identical clauses. After the crisis began, clients would need to know what the contract said about e.g. insolvency. So they would have to dig out the derivatives contract, from thousands, flick to the right page to find the insolvency clause. Or they needed to know whether the contract was signed. So they would have to dig out the derivatives contract, from thousands, flick to the right page and check whether it was signed etc. She said a simple monitoring program which could have automated this would have saved them hours of time but the problem was this was how derivatives had always been done and change is a difficult thing to push in law firms.

Fuse works with all departments of A&O and encourages them all to work with the tech companies and try to create something, with the end goal to try to develop a better work/life balance for their lawyers and attempt to cut down on the 60/70/80 hour week by moving the time-consuming manual labour over to technology.

Last up in the session was Julia Salasky, (founder of CrowdJustice) who worked for Linklaters and the UN before growing frustrated with the lack of creativity with which she was able to do her work. Everything is very much how it has always been, so she wanted to do something differently. She spoke a lot about having an entrepreneurial attitude and what that means; she basically boiled her most important lessons down to not being afraid to fail and accepting that there are some fires which you can’t put out as you work. Sometimes you have to let the fires in the business burn whilst you concentrate on other areas.

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

Session 2

The second morning session talked about the skills that the next generation of lawyers need/the current missed when they were hired. It featured research from BPP and talks from Jo-Anne Pugh (Director of Strategic Design at BPP), Adam Corphey (Head of Innovation Technology at BPP) and Mark Collins (Global Head of Knowledge Management at Herbert Smith).

They had conducted research before the conference with 77 legal entitites (inc. Global firms, National firms, Regional firms, Small/Boutique, in-house etc) to find out exactly what they felt were missing. The 9 areas they highlighted for future candidates, with the ones they chose as most important in bold, are:

- Commerciality – i.e. commercial awareness, understanding the law firm is a business, understanding business trends etc

- Tech/Digital skills – i.e. the ability to analyse tech and data, awareness of lawtech (with exposure to it a big plus in their eyes – you can get exposure by heading to demo events etc)

- Written Communication – Interestingly, they said written communication is a major area which needs improvement upon hiring. They said the ability to write concisely with attention to detail just isn’t there in new hires, even when simply drafting written comms in the form of emails, and they spend a lot of time developing this.

- Client facing skills – Personally think it’s a bit of a weird one for them to have highlighted. It doesn’t seem an area that students can work on that heavily? Maybe Jaysen will disagree and come up with examples of how to develop these skills but personally believe this is something which law firms should expect to teach, not expect future candidates to have.

- Flexibility & Resilience – I think probably obvious that adaptability is a big skill to be sought out by firms at the moment. With Lawtech & the SQE coming in, there seems a lot of change to be afoot in the legal industry and they want candidates that they feel can deal with this.

- Professionalism – Not just how you present yourself at interviews (appearance, etiquette etc) but also other areas too such as your social media presence, as social media begins to play a bigger part of day-to-day professional life and moves away from being a totally separate entity.

- Time & Self-management – Law firms want, more and more, someone who can demonstrate that they can manage themselves and their time effectively. They mentioned examples such as demonstrating project management skills (even on a small scale such as planning and organisation of group activities).

- Teamwork – They highlighted the various real functions of what they meant by this. They don’t just mean playing in your local football team but rather displaying emotional intelligence and a desire to work within a team to better serve firms who are, increasingly, working across business functions with mixed teams.They also said email has begun to destroy internal social interactions and they want candidates who would prefer to walk across the office and actually talk to the person they need to.

- Creativity – The final skill they selected as important, they want candidates who are creative and have new ways of thinking. Try to figure out ways of displaying this on your application but, also, take it with a pinch of salt given I’m not entirely convinced they mean they want an entirely new breed of candidate, rather a slightly creative variant on the ones they get now.

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

Session 3

The afternoon session had an intense two hour session on the SQE.

To begin with Julie Brannan (Director of Education at SRA) began with a discussion about why the SQE is necessary. She highlighted the big drop-off of student numbers between graduation with a law degree and commencing the LPC, pushing forwards the idea that whilst some of these graduates will have simply chosen a career outside of traditional law, it is unacceptable that the current method of LPC/TC means many will simply not be in a position to take a gamble, thus those of a certain social class will be discouraged from pursuing a career in law. She also highlighted the LPC pass-rate of white candidates (80%), Asian candidates (50%) and Black candidates (40%) as further proof that change is necessary to try to counter-balance the current situation.

However, details were light on the ground as to what the SQE will consist of. We know it’ll be 2 parts with 2 years of qualifying experience necessary. The 2nd part may be more focused on practical skills picked up by the experience, so in theory it would be done at the end of the qualifying period. The qualifying period is still up in the air, but it seems experience gained under the supervision of a qualified solicitor will be enough. In short; the SQE is coming but nobody seems to know what it’ll be.

After this it got fun (or irritiating depending on which side of the fence you sit on) as Thom Brooks (Dean of Durham Law School) had a rant about how the SQE is similar to Brexit – nobody asked for it and the details as to how it’ll happen are nil; SQE means SQE. After this, Richard Moorhead (Chair of Law & Professional Ethics at UCL) stood up and similarly offered a criticism of the SQE; how nobody really knows what is going to happen or what the effect will be. He called for a slow transition into it, a testing of areas alongside the current system. Crispin Rapinet (Training Principal at Hogan Lovells) similarly echoed the criticisms of this approach to change within the industry. He stated it’s impossible to move forwards and plan without any detail.

Maeve Lavelle (Director of Education & Community Programmes at Neota Logic) offered a different perspective on the SQE’s introduction, talking about how change is necessary within the industry from both a social perspective (given the increasing lack of access to justice but also diversity issues within law) as well as discussing the need for cognitive diversity within the industry, which is unlikely to happen quickly or at all if change isn’t embraced.

After this we heard more of the same criticisms of the SQE from Chris Howard (Professor of Legal Education at KCL), a discussion on the importance of pro bono projects from Linden Thomas (CEPLER Manager at Birmingham Uni) and a general talk about the value of a law degree from Andrew Francis (Professor of Law at Leeds Uni).

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

Session 4

The final session of the day was quite interesting and featured a panel discussion of apprenticeships are affecting other industries and what training/development is happening within them. Euan Blair (CEO of Whitehat), Keily Blair (Director of Regulatory & Commercial Disputes/Head of Legal Training at PwC), Iain Gallagher (Senior Manager of Emerging Talent at Santander), Sam Harper (GC at Deliveroo) and Samuel Gordon (Research Analyst at Institute of Student Employers) had a general discussion about the pros and cons of apprenticeships, and whether the legal sector would introduce them or not. I’m not really going to detail out the points because my notes are pretty crap from this section of the day and also I’m not sure how relevant it’d be to you lot given your aspirations but the end takeaway from this session was that apprenticeships can be great or terrible, it depends on the person. More firms should do it as it can encourage social mobility far more than most other initiatives but it seems unlikely we’ll see the legal sector introduce them in any meaningful manner.

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

Final thoughts

To be honest with you guys, it was a really great event and I was pretty lucky to be brought along to it. A lot of influential people were there to speak to and a lot of differing opinions to be heard.

The one thing that really struck me though was made apparent in Session 3. A lot of people talk about the need for change in the industry but when it comes down to it, people don’t really want it to happen because it may threaten what they have now. I got the impression, from sitting in that room and listening to senior legal figures mocking the SQE and the SRA within the safe confines of the echo chamber of the conference, that it didn’t matter what changes were really submitted, if they were wholesale then they would find criticisms of it and paint it as bad.

Not to try to defend the SRA, as I think they’re doing a pretty poor job of selling the SQE given the total lack of information they are releasing, but I think the approach they’re taking (drastic changes) are a better way of doing it than minor tweaks here and there. There isn’t much to dispute that the current system favours a certain background (ethnic, class and educational) and that this needs to be combated. A major overhaul followed by tweaks to actually make it work is, in my opinion, a more realistic approach to solving the current issue than to try it the other way round.

Anyway, thought I’d throw my two cents in at the end there, hopefully there is some information within this entire post that people find useful on how law firms are thinking about the future.

[divider height=”30″ style=”default” line=”default” themecolor=”1″]

[blog_teaser title=”” title_tag=”h3″ category=”” category_multi=”” margin=”1″]

Commercial Awareness Briefing – Part 2

Welcome to Part 2 of our commercial awareness summary for March and April 2018. If you missed our last email, you can access it here.

We are currently preparing mock case studies that mirror the written exercise at assessment centres. If you’d like a copy, please sign up to our forums as we’ll be circulating them over there very soon.

Have a good week!

![]()

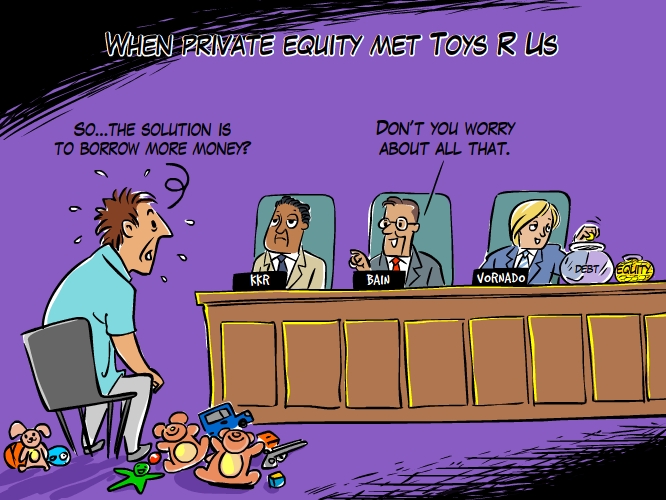

Toys R Us

Goodbye to Toys R Us

- The story: Toys R Us is closing all of its UK and US stores. In the US, the company filed for bankruptcy, whilst in the UK, the company went into administration. Administrators of the UK arm were unable to find a buyer.

- Impact on law firms and clients: This story reflects two broader points. First, Toys R Us is one of a series of traditional businesses that have had to close in light of the rise of e-commerce platforms such as Amazon. Second, the fall of Toys R Us reflects the dangers of taking on too much debt. Toys R Us was bought by private equity firms in 2005 and they piled debt onto the business to expand internationally. Toys R Us could not keep up with the payments.Other UK retailers have suffered including Maplin Electronics, which went into administration after failing to secure a rescue deal. This is a busy time for restructuring and insolvency lawyers, many of whom predicted the collapse of the high street. Kirkland & Ellis advised Toys R Us in the US and UK, whilst an Eversheds team advised Maplin.

Russia

Putin’s landslide victory

- The story: Russia’s president won a landslide victory in the Russian elections with an estimated 75.6% of the vote. His campaign spokesman partly thanked the UK, linking the record voter turnout with the UK’s accusations against Russia. Britain recently expelled 23 diplomats and blamed Russia for the use of a nerve agent against a former double agent, Mr Skripal, something that Russia has vehemently denied.

- Impact on law firms and clients: In the short term, this political uncertainty is bad for the markets as companies slow down investment at times of unrest. If it escalates, the sanctions could further squeeze the Russian economy and affect both investment in and investment out the country. A few law firms are currently based in Russia including A&O and White & Case, and they may need to help restructure targeted Russian companies.

The other side of trade with Russia

- The story: Despite the political chaos between the UK and Russia, companies in both countries don’t seem to have had much problem trading with each other. Gazprom recently issued a $750m eurobond in London and the Russian government issued a $4bn bond in London.

- Impact on law firms and clients: In the public markets, there are 57 mainly-Russian companies listed on the London Stock Exchange, the most for any country outside Moscow. A number of MPs have also taken positions working for or acting on the boards of Russian companies. Lawyers are cautious about how the political climate will affect their Russian clients. Many think it will sort itself out, but some banks have limited Russian business and some investors are concerned about the impact on wealthy Russian clients. If they move this could impact legal work for private clients and Russian businesses. Fun fact – last year, the wife of the former deputy finance minister to Mr Putin paid £160,000 to play tennis with Boris Johnson!

Severe sanctions from the US

- The story: The US government announced its latest round of sanctions against Russia on Friday. They targeted prominent Russian billionaires, government or state-owned officials, and companies. This is the US’s toughest sanctions against Russia to date.

- Impact on law firms and clients: Many Russian companies have been hit hard. Shares in EN+ fell 22% and shares in Rusal fell 18%. Rusal later released a statement to say it is consulting with its legal advisers on the next steps. This is going to affect a range of companies that trade with Russian multinationals, for example, EN+, which is listed in London. Depending on how long it lasts, companies may be advised to consider finding alternative suppliers.

M&A

Global dealmaking passed $1 trillion at fastest pace

- The story: In a signal of how well M&A is doing globally, the total value of deals passed $1 trillion in record time. In the UK and Japan, M&A dealmaking volume is double the rate of last year and in Germany, it is four times higher. Value is also up a lot in a sign that private equity firms are confident to do bigger deals.

- Impact on law firms and clients: M&A and private equity teams are going to be really busy as it looks to reach record levels this year. Law firms may bulk up their teams by external hires or make more partner promotions within corporate.

M&A activity continues to break records

- The story: Despite tariffs, Brexit, protectionism and global political concerns, M&A continues at a record rate up 67% from the same quarter last year.

- Impact on law firms and clients: There has also been a large increase in big transactions as companies move to beat the disruption of technology. European deal volumes have almost doubled from last year, especially in private equity. For example, Carlyle recently acquired Akzo Nobel’s chemical business in one of the largest European PE deals in recent years. For that deal, Latham & Watkins is providing the corporate advice in London and finance advice in the US, a sign of the benefits of having a strong presence in both jurisdictions to secure places on the biggest deals. At the same time, Chinese overseas dealmaking has slowed to the lowest since 2005, a clear sign of the consequence of Trump’s trade policies on M&A.

The big hostile takeover

- The story: Investment firm, Melrose Industries, has been in a battle for the last two months to try to buy GKN, one of Britain’s oldest engineering companies. This is despite sustained criticism by many politicians, customers and trustees. Recently Airbus, its biggest customer, said it would be difficult to work with the company if it was acquired. Airbus noted that they want to work with a supplier that invests in the UK for the long term – not one that is looking to break up the company and sell. 16 MPs have also written to the business secretary asking the government to block it on grounds of national security.

- Impact on law firms and clients: The government can block an attempted acquisition under the 2002 Enterprise Act on public interest grounds. This is something the US government did when Trump stopped the attempted acquisition of Qualcomm.

Update to Melrose bid for GKN

- The story: Elliot Advisers, the UK arm of a hedge fund that owns over 3.8% of GKN said it plans to vote in favour of Melrose’s offer to buy GKN for £8bn. They called for other shareholders to do the same. David Cumming, chief investment officer at Aviva, has also backed the bid. There are four days left before the shareholders have to decide.

- Impact on law firms and clients: This has been called the most hostile takeover in decades. Whilst, Melrose now has public support of roughly 10% of GKN’s shareholders, many have called on the regulators to intervene and asked the government to legislate to protect British businesses. This comes as Unilever moved its headquarters from London to Rotterdam because of its tougher rules against hostile takeovers.

Melrose buys GKN

- The story: The vote took place yesterday and a majority of GKN shareholders agreed to sell their shares to Melrose in a £7.9bn cash and shares offer. This was helped by the fact that a substantial minority of the shares were held by hedge funds.

- Impact on law firms and clients: The close vote (52.43%) reflects the uncertainty of buying long established UK companies. But the battle isn’t over yet, the business secretary made Melrose agree to the government’s right to veto the sale. It’s now up to the government to determine whether there are public interest concerns. This agreement is something that has become more commonplace since the Kraft-Cadbury deal but the government has never been so public in its involvement. Meanwhile, some have called for a review of UK takeover laws over concerns that existing legislation does not adequately protect longstanding British businesses.

Trump blocked the biggest even technology deal

- The story: Trump has blocked Broadcom’s attempted $142bn acquisition of Qualcomm. Both are chipmakers and Apple is a key client of Broadcom. This is the first time a president has blocked a deal over national security fears. Trump’s administration reportedly feared that the acquisition would pave the way for China to lead the growth of 5G wireless technology.

- Impact on law firms and clients: This was a hostile takeover and would have made a lot of money for legal advisers in M&A and finance. Broadcom’s advisers included Latham & Watkins and Wachtell Lipton Rosen & Katz, whilst Paul Weiss, DLA Piper and Allen & Overy were favoured to act for Qualcomm. It comes as regulators are increasingly worried about foreign takeovers by Chinese companies, which may cause law firms to see a fall in outbound Chinese M&A deals.

Trump’s tariffs

- The story: Trump’s advisers originally came up with $30 billion of tariffs to target China but Trump ordered them to double it – so now there is going to be $60 billion worth of annual tariffs. China said that whilst don’t want a trade war, they will fight back and they’ve prepared retaliatory tariffs on 128 US products. China has faced internal pressure to go even tougher and target US soybeans, aircraft and cars but it remains to be seen what their next steps are.

- Impact on law firms and clients: Japan was seen as the first tragedy of the US-China trade war as Japanese stocks fell and the yen rose. Trump decided not to exempt Japan from tariffs aimed at China, which could significantly damage profits as many Japanese companies are dependent on exports. Stocks have also been affected: US stocks had their worst week in more than two years and European shares fell sharply. The news particularly hit banks and companies that do a lot of global trade. Deutsche Bank hit their lowest level since late 2016 and Boeing has seen shares fall 10% as the company is heavily reliant on supply chains in China. Lawyers may advise companies to slow down on investments and consider their supply routes between the US and China.

Trump’s escalating trade war

- The story: In response to alleged intellectual property theft, the US government has announced plans for a 25% tariff on 1,333 Chinese products. The products include robots, vaccines, electric cars and military weapons. It also features components that US companies may use. China responded quickly with a 25% tariff on 106 products, which includes cars, soybeans and some aeroplanes.

- Impact on law firms and clients: This is going to impact many US manufacturers and US-China trade relations. The growing trade war hurts companies looking to invest in the US and China, and companies that rely on international trade. Law firms have already found it hard to operate in China and they may have to reconsider their expansion plans if this continues to escalate.

And another retaliation…

- The story: It didn’t take long for Donald Trump to respond to the recent Chinese tariffs. He has called for tariffs on an additional $100bn of Chinese imports.

- Impact on law firms and clients: It’s clear that Trump won’t be the one backing down from this escalating trade war. The US, EU and Japan have also joined the US in a case against China’s alleged intellectual property theft at the World Trade Organisation. In many ways, the integrity of the WTO is at stake, especially if other nations decide not to follow international trading standards. Meanwhile, financial institutions have had different responses. BNP Paribas noted that there are risks to the Chinese banking system and little to benefit from a trade war. Blackrock said it’s an opportunity for negotiations with China. Whilst UBS warned clients about the risk to global growth.

Trump reconsidering trade agreement

- The story: Trump is said to be looking to rejoin the Trans-Pacific Partnership provided he sees a better deal for the US than before. Trump originally withdrew from the TPP after coming into power.

- Impact on law firms and clients: The TPP is an agreement between 12 countries to cut tariffs and create rules for international trading. The aim is to stop China from setting trade practices across the world by creating uniform rules in many areas like intellectual property, patents, employment and the environment. It’ll also bring new opportunities for businesses and may force some countries to get their laws up to speed. This could mean more legal certainty for businesses operating in those jurisdictions. It could also mean more avenues for litigation teams because companies can sue governments for laws that affect them.

Gender pay reports

- The story: More firms have now submitted their gender pay gap figures under government requirements. These require employers with over 250 employees to publish gender pay. So far, of the reported companies, 3 out of 4 pay men more than women, with some of the biggest gaps are in financial services. But some have criticised the governments reporting measures because it overlooks a lot of factors that determine pay.

- Impact on law firms and clients: The public reporting has forced companies to come to terms with their gender pay gaps. For example, EY’s graduate intake is at 58%. But the problems arise going up the ladder – 80% of EY’s partners are male. Employers may be worried about the impact on their brand. Easyjet, for example, had a 45.5% gap but compensated by presenting the data early and explaining clearly what they were doing to improve, such as clear targets. Law firms have also reported their figures but some have called the picture distorted because they don’t have to reveal partnership data – where the gap is likely to be the highest. Some law firms voluntarily included partnership data including Clifford Chance, reporting a 66.3% gap. The firm also called out others to do the same. This prompted Linklaters, which originally reported a figure of 23% for non-partners, to revise their figures to 60.3% when including partners. Comparing the figures for non-partners, out of the magic circle, Linklaters has the highest mean hourly pay gap and Freshfields has the lowest (including one of the lowest out of all the reported firms).

Stock Market

Spotify flotation

- The story: Spotify listed on the New York Stock Exchange and was valued at $26.5bn. The company didn’t go for a normal flotation in a sign of the uncertainty around tech stocks at the moment. Instead of hiring a bank and going through an extensive IPO process, Spotify went direct to the market to sell existing shares.

- Impact on law firms and clients: The recent tech sell-off in the stock market has shaken a lot of investors and caused prices to fluctuate a lot in recent weeks. This may reflect a broader concern about IPOs and companies may put flotations on hold over fears about the current political climate. It also shows the alternative means to access the equity capital markets. Spotify’s route to the market, a direct listing, is seen as a test case for future companies.

Avast aiming for one of the largest tech flotations on the London Stock Exchange

- The story: Avast, one of the world’s largest cyber security companies operating direct to consumer, is planning to raise $200m in an IPO. Existing shareholders will be selling shares in the company, which is backed by the private equity firm CVC Partners.

- Impact on law firms and clients: Avast chose to list in London rather than New York in a sign of the competitiveness of the LSE despite concerns over Brexit. It also comes as the cyber security market is expected to grow rapidly over the next few years as companies and law firms are trying to build systems to better protect themselves from hackers. The number of IPOs backed by private equity firms is also expected to grow a lot this year.

US economy

Inflation and wage risks to the US economy

- The story: The CEO of JP Morgan released his annual letter this week and commented on the risks of the US economy overheating because of higher inflation and wages. He suggested that the Federal Reserve may have to take ‘drastic action’ by raising interest rates quicker than anticipated.

- Impact on law firms and clients: This one is a mixed bag. The suggestions that there are dangers in the US economy comes from the fact that it is growing well, but potentially too fast. Whilst M&A and banking will be busy, firms need to prepare for the risks that the Federal Reserve does step in and raise interest rates. That’s a problem if many companies are borrowing to finance their activities whilst the interest rates are low.

US investment banks earnings report

- The story: JPMorgan, Wells Fargo and Citigroup are releasing their earnings for the first-quarter today. This will give an idea of the strength of the lending market, the impact of US volatility and how lighter regulations will impact their balance sheets.

- Impact on law firms and clients: It’s hoped that bank earnings will help to stabilise the market as many investors are concerned about a trade war, the Middle East and US politics. If it doesn’t rally the market, there are concerns about the future of the US economy and its ability to handle this uncertainty.

March and April’s 2018 Commercial Awareness Update

Welcome to our bi-weekly commercial awareness newsletter. Over the coming months, we will be breaking down a range of case study questions and topical business issues. For more details, please check out our recent forum post.

Today’s post is a little different. One of our members has been posting useful commercial awareness updates in our forums over the last few months. We wanted to share.

If you’ve fallen behind on the news or just want to refresh your memory before an upcoming interview, we have collated the posts below. Note, we’ve broken down the summaries into two newsletters, so this is part 1 of 2.

Big props to Coralin for improving her commercial awareness! You can find the full posts – in date order – for March here and April here.

![]()

The General Data Protection Regulation (“GDPR”)

- The story: The GDPR – an EU regulation that’s considered to be ‘the biggest overhaul of the world’s privacy rules‘ – comes into force on the 25th May 2018. It will regulate how companies use the personal data of EU citizens. So, if you’re a company that collects personal data, you’ll need to make sure that you’re compliant, or you could be subject to some very serious enforcement measures. Regulators will have the power to fine companies to the highest of €20m or 4% of a company’s annual turnover – whichever is higher.

- The Federation of Small Businesses reported that fewer than 1 in 10 small businesses in Britain are prepared for the General Data Protection Regulation. The group has called for a safe harbour so businesses can get advice rather than face a penalty if they don’t comply immediately. The GDPR adds stricter rules on processing and personal data storage, and includes new consent requirements. Businesses that have lots of personal data will also need to appoint a data protection officer.

- Impact on law firms and clients: This regulation is going to significantly impact law firms, directly and indirectly. Both companies and law firms will be required to follow stringent rules on how they process and store data, and whether they get customer consent to use the data. The reach is also wide. In addition to companies operating in the EU, the regulation applies to those who employ EU workers or sell to EU customers. Regulatory and data protection lawyers who specialise in this field will be in high demand as companies will need detailed advice to avoid the significant penalties. The problem for many small businesses is that compliance is costly, and many can’t afford to hire lawyers to help. It could impact the ability to do business.

Brexit

Unilever is leaving the UK

- The story: The company behind big brands like Magnum ice cream, Persil, Marmite and Dove has chosen Rotterdam instead of London for its new headquarters. Some, including the shadow business secretary, has used this to suggest businesses ‘are losing confidence in the government’. But both Theresa May and Unilever have said it is not related to Brexit. In fact, Unilever has said it will continue to invest £1bn in the UK. Unilever has been in the UK for 130 years and it’s the third biggest UK company by market value (valued at £105bn!).

- Impact on law firms and clients: Many think the move is because the Netherlands has stricter protectionist rules that can prevent foreign takeovers. We’ve seen a recent example of this – the acquisition of British engineering company GKN by Melrose. And this comes after Kraft Heinz tried to buy Unilever last year. Unilever will require law firms to help with their restructuring and relocation. It remains to be seen whether Slaughters – the company’s longstanding adviser – will be chosen, especially because Linklaters has acted for Unilever recently. Whichever firm is chosen, the company will need the advice of Dutch counsel for the move.

Brexit transition and financial services

- The story: The EU agreed to a 21-month transition period for Brexit after Theresa May agreed to pay an exit bill (£35-39bn!). Many predict that the detailed negotiations won’t begin until next March, and that means an exit won’t take place until the end of 2020. Financial services were also mentioned in the European Council’s draft negotiating guidelines for the first time. Part of this is thanks to Luxembourg, which has a lot of links to London when it comes to financial services. Contrast this to France who has played hardball, refusing to give the UK a special deal for financial services. It’s clear that France’s financial services stand to gain a lot with the UK out the picture.

- Impact on law firms and clients: The wording if the draft negotiating guidelines says that financial services in London will get the same access as any other non-EU country. This suggests banks and companies won’t get the same passporting rights that they had before Brexit – or any special provisions altogether. This will have huge consequences as currently many companies use the UK as a platform to enter into the EU. As it stands, this will limited. Expect law firms to establish Brexit teams and provide resources to help companies with preparations and appropriate contract provisions. Meanwhile, the European Central Bank is still advising EU banks to assume a worst case scenario, suggesting that they undertake contingency planning. Some companies have been preparing for the loss of passporting rights for some time now. Investment banks such as Deutsche Bank and Goldman Sachs have already started moving people out of London. They’ll need law firms to relocate and restructure.

PSA to stay after Brexit

- The story: PSA, the parent of car companies like Vauxhall, Peugeot and Citroen, is going to continue to manufacture vehicles until at least 2029. This follows a £9m investment by the UK to guarantee its competitiveness after Brexit.

- Impact on law firms and clients: The UK’s investment gives some certainty to carmakers on what’s going to happen after Brexit. It’s a sign of how interlinked the industry is with the EU as over half of vehicles that are made in the UK are exported to the EU and over half of the manufacturing parts come from the EU. That’s interesting to think about with the threat of a trade war on the horizon – I’ve discussed this in Part 2 of the Commercial Awareness Briefing.

.

Tech companies

Digital Tax

- The story: Next week, the European Commission will propose a 3% ‘digital tax’ on many technology giants including Google, Spotify, Facebook and Apple. It’s difficult to say whether it will be implemented because all member states need to agree. For example, Ireland, known for its lax tax regime, opposed the bill, and it has been heavily criticised by the US.

- Impact on law firms and clients: If companies are uncertain about their tax liabilities, they may seek out help from tax lawyers about how to better structure their business. But note, law firms will need to be careful that they are complying with the law and not helping companies to avoid tax(!). Big US tech companies may think about relocating if this is implemented.

Tech stocks back up

- The story: Tech stocks have been falling for a while now, especially since the Facebook scandal. To add to the heat, Trump’s comments on Amazon has also rocked the markets. You may have heard that Trump criticised Amazon for paying minimal taxes. But it gets worse. A report came out suggesting Trump is ‘obsessed’ with sorting out Amazon. This news caused Amazon’s shares to fall up to 4.6%; it’s a clear example of how politics can affect companies. Meanwhile, in China, policies have been approved to encourage big tech companies to list on their stock exchange. A number of companies have already said they are interested in listing in China.

- Impact on law firms and clients: Investors may need to be careful; many people appear to be heavily invested in tech stocks, which leaves them vulnerable to events like this. Before this, technology stocks were rising for a long time, leading to many concerns that they could be in a bubble. Many were also concerned about the high valuations for tech startups – so-called unicorns – that were valued at over $1bn. Investor fears continue over the regulation of tech companies, partly contributing to the S&P 500, featuring some of the biggest US companies, to suffer its first quarterly losses since 2015. In relation to the China story, law firms may consider entering China now if they haven’t already. If they can eventually practice local law, the capital markets will be a very popular practice area.

The Japan Fair Trade Commission has raided Amazon

- The story: Japan’s regulator has raided Amazon’s Tokyo headquarters. The company is being investigated for requiring suppliers to absorb the costs for its discounts. A similar issue happened in 2016 when the Japan’s Fair Trade Commission found Amazon had forced suppliers to sell items at the same or a lower price on the company’s website. Two years ago, Amazon took over its rival company in Japan, making the country Amazon’s third biggest market (interestingly German is second, not the UK).

- Impact on law firms and clients: These practices are against Japan’s antitrust laws, which prevent firms with a better bargaining position taking advantage of its partner. Lawyers will have to review contracts and Amazon may have to change its supplier agreements to ensure the company complies with the law. This story reflects the wider problem of regulators trying to regulate companies that have reached an unprecedented size. Some expect Amazon to become the world’s first trillion dollar company.

Amazon becomes second most valuable company

- The story: Amazon became the most valuable company early this week beating Alphabet, Google’s parent company, who was in second place. Amazon now sits just after Apple. The company has had a good few years, and it’s share price has surged after the acquisition of Whole Foods, Just recently, Amazon overtook Google as the world’s most valuable brand.

- Impact on law firms and clients: Google suffered after the Facebook data scandal because investors were concerned about the risk of new data regulation. This would impact their profits because Google’s advertising model centres around the use of data.

Facebook’s political scandal

- The story: Facebook is under fire after it was leaked that Cambridge Analytics, a company which claims to ‘change audience behaviours’, used data obtained from Facebook users without their consent. This was under the guise of a personality test, using an app called “This is your Digital Life”, which was downloaded by hundreds of thousands of people. The harvested data was then used for political targeting in the Trump election campaign. It was an employee at Cambridge Analytics, Christopher Wylie, who released the information. He was a former law student(!) and coder.

- Impact on law firms and clients: Data protection is increasingly on the agenda and the question for Facebook is – how far should companies go to protect sensitive data? Interestingly, what Facebook did wouldn’t be illegal in the US – companies can share third-party information. So the issue is that it is illegal under EU data protection law, which shows the differences between the stricter regulation in the EU and the lax position in the US. It also comes as companies like Facebook will have to prepare for the General Data Protection Regulation, which comes into force in May. Regulators can enforce big penalties for failing to report breaches (which is what FB seems to have done), so if there are more reveals, Facebook could become under fire. This story also follows news that Facebook allegedly failed to prevent Russian operatives from creating fake accounts and influencing the US elections. In the UK, the data watchdog is looking into it and contacting other analytics companies to see how data is being used.

The economic damage of scandals

- The story: $60bn was wiped off Facebook’s market value last week, a huge amount of wealth for Mark Zuckerberg, in a sign of how damaging the Cambridge Analytics scandal has been. Investors have been worried about fines and the loss of users, which show privacy fears are costing Facebook. Sonos pulled advertising from Facebook, Instagram, Google and Twitter for a week. Mozilla and Commerzbank also put advertising on hold. Investors have also withdrawn from tech stocks amid a big sell-off. Facebook’s control of personal data is now in the public eye and many have called for tougher regulation – a move that is likely to affect many business models.

- Impact on law firms and clients: This was an interesting story from a commercial awareness perspective. Many regulators in the EU and US are looking at how to regulate data companies. And this isn’t the first time. In 2014, the EU fined Facebook for providing misleading information about the ability to merge information between Facebook and WhatsApp. Last month, the EU also ordered Facebook to stop tracking people who aren’t using Facebook as they browse the web(!).In addition to the GDPR in May, the EU is discussing an e-privacy directive which, if passed, would significantly restrict the tracking of users’ behaviour online. Some investors fear that companies with similar data on users could face more regulation. Indeed, Google and Facebook’s value is largely based on the use of huge amounts of personal data. If this follows to other data companies, law firms may decide to invest in data protection teams. These lawyers can help advise these companies to comply with the regulation and mitigate against the risk of strict enforcement measures.Interestingly, some practices in the US are illegal in the EU, which shows the divergence in policy between the two. For example, Facebook’s Messenger for Kids would not be allowed in the EU due to age restrictions.

Background to the Cambridge Analytica scandal

- The story: We now have more information about the Cambridge Analytica scandal. Aleksandr Kogan, the Cambridge Analytica contractor at the heart of the Facebook scandal, was an employee of the Cambridge Psychometrics Centre. It was there that his team discovered they could use social media to determine people’s psychological profiles. Kogan then created an app called “This is your Digital Life”, a personality quiz for Facebook users. It was a success – 270,000 users signed up, but that wasn’t the whole story. Facebook’s privacy settings allowed Kogan to access the data from each user’s Facebook friends. This meant he could harvest a lot of data: some estimates suggest that he was able to build profiles of 50 million people. Kogan then gave this data to Cambridge Analytica. Meanwhile, an undercover investigation by Channel 4 into Cambridge Analytica was very revealing. The CEO was recorded discussing the company’s history of bribing politicians and spreading ‘fake news’.

- Impact on law firms and clients: There are increasing concerns about how personal data is being used to influence behaviours. This could lead to more regulation for companies that use data to market their products and perhaps this could go so far to target supermarkets that store shopping data using discount cards. At this point, companies will be checking that they are compliant and may need the help of law firms to ensure they have clear policies.

Facebook in trouble

- The story: The EU justice commission will be speaking with Facebook’s COO, Sheryl Sandberg after finding that Facebook’s written response “fell short” of their expectations.

- Impact on law firms and clients: Whilst this is a small story, there are some broader commercial awareness points we can draw from this. Europe’s data protection laws are some world’s toughest and very different to the US. Whilst the public outcry against Facebook is universal, there are concerns that the EU will pressurise US companies to improve privacy standards. So law firms need to be on guard – this is a very hot topic at the moment.

You can find Part 2 of the commercial awareness briefing here.